A buyback of shares is a financial plan where a company repurchases its own shares from shareholders, reducing the number of outstanding shares of the company. This measure can increase the value of the remaining shares and enhance the company’s financial ratios. Buyback shares of the company are used to rationalize the capital of the company, and, in today’s business environment, it also serves as a crucial avenue to offer an exit option to the investors.

According to the Companies Act, 2013, buybacks must be financed through (i) free reserves, (ii) issuance of new shares (different from the ones repurchased), or (iii) the securities premium account of the company.

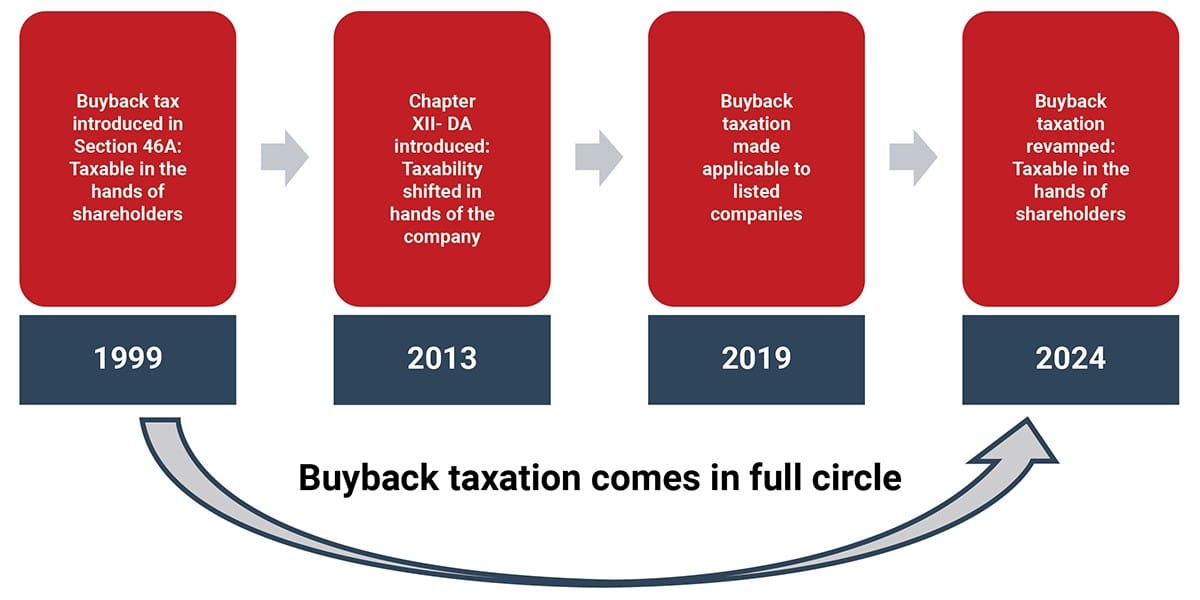

As per the Finance Act (No. 2) 2024 from October 1, 2024, new regulations on tax for buybacks of shares will be implemented, transferring the income tax liability from companies to shareholders. These changes will now impact companies’ pattern of allocating capital and the investment plans of companies. Let us examine who stands to gain from these changes and analyze them. tax landscape surrounding buybacks has undergone significant transformation over the years. Currently, an Indian company undertaking buyback before October 1, 2024, is required to pay income tax on the amount of ‘distributed income’ (i.e. difference between the consideration paid to the shareholder in the buyback and the amount received by the company for the issuance of such shares) at an effective tax rate of 23.30% (including surcharge and cess). Further, income tax provides for an exemption to the shareholders in respect of the consideration received by them towards the buyback from the company. From October 1, 2024, according to an amendment in buyback tax introduced by the Finance Act (No.2) 2024, there have been substantial changes in the taxation system for buybacks wherein the tax obligation has been switched from the hands of the company to the hands of the shareholders, altering the existing system entirely. In the current regime, the dividend is taxable in the hands of the recipient as per the applicable tax rates, which may go as high as ~36% as compared to buyback tax which is taxed ~23%. Also, the surcharge rate on buyback tax was restricted to 12% as compared to 15% for dividend income. Further, under the existing regime, buyback tax is levied on the distribution amount as reduced by the consideration received for shares issued, whereas in the amendment such amount is deferred as carry forward losses. For an individual promoter subject to the highest slab rate, net cash flow will significantly decrease due to the proposed amendment. Meanwhile, for a company taxed at approximately 25% or 29%, the difference between pre and post amendment, though smaller, remains considerable with respect to cash flow. Resident investors Non-resident investors Additionally, if the shares bought back by a non-resident shareholder are held by them as ‘stock-in-trade’, the proceeds from the buyback may be treated as ‘business profits’. The taxability of business profits depends on whether the non-resident shareholder has a Permanent Establishment (PE) in accordance with the relevant tax treaty provisions and Place of Effective Management (PoEM) under the Income Tax. Interestingly, changes in the buyback tax regime presents distinct advantages for certain groups. In conclusion, while the legislative amendments are intended to equalize the taxation on dividends and buybacks, their practical implementation may lead to considerable challenges. The increased tax rate on buyback proceeds in the year of receipt and the potential for capital loss set offs against any capital gains may reduce the appeal of buybacks. Companies often utilize share buybacks to reward shareholders and provide an exit for minority shareholders without engaging in the NCLT process. However, with the new amendments, these provisions have become less appealing. These unintended outcomes highlight the necessity for a re-evaluation and possibly redesign the buyback tax regulations. Proactively addressing these concerns is crucial for ensuring that the legislative intent is achieved without adding extra burden on the taxpayers. Making the buyback provision more attractive from a tax standpoint would benefit all stakeholders. Authored by:

Evolution of Buyback Tax Overtime

Buyback Taxation Post Finance Act 2024

The tentative tax outflow for domestic investor pre and post amendment scenarios has been tabulated below

Particular

Existing law upto 30 September 2024

Buyback law as applicable from 1 October 2024

Tax incidence in hands of

Company (exempt in hands of shareholders)

Shareholders

The rate of tax deducted by the company on buyback income

23.92%

Not applicable

Maximum rate of tax at which the buyback income is taxable in the hands of resident shareholders

Exempt

35.88%

Whether any withholding tax to be deducted by the company at the time of buyback in case of resident shareholders

No

At 10%

Maximum rate of tax at which the buyback income is taxable in the hands of non-resident shareholders

Exempt

23.92% (subject to treaty benefits, if any)

Head of income under which buyback proceeds are taxable

Exempt

Income from other source

Treatment of cost of acquiring shares tendered in buyback under the Income Tax Act

Not allowed as capital loss

Treated as capital loss which can be set off against any other capital gain income.

Impact Analysis

Who Benefits from the Changes?

Conclusion

Megha Gala | Direct TaxFrequently Asked Questions (FAQs) on Buyback Tax Reforms